In my last article, we saw why it is necessary to have family health insurance, not less than 25 Lakhs. We also saw that if we consider inflation for the next 5 years, it is necessary to have health insurance, not less than 50 to 60 Lakhs.

( Please click the below link to read my last article: http://malaychitalia.home.blog/2019/04/18/what-should-be-your-familys-health-insurance-amount/ )

But now the question arises, this much of Health Insurance will cost a huge amount of premium also; how will we manage this?

The answer is negative. Nowadays, it has become easy to get high-value health insurance at a very reasonable premium. Since last few years, a new concept has been introduced to the market which is called “Super Top-up Plans”.

Now, what is “Super Top-up Plans”? Let us understand this systematically.

[youtube https://www.youtube.com/watch?v=hfxAaDOQOkg&w=560&h=315]

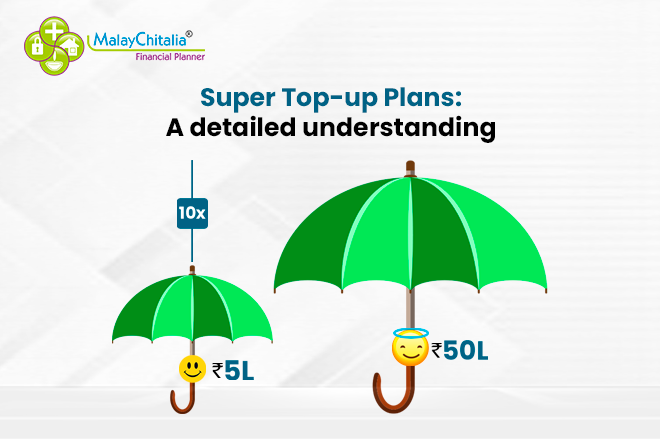

For understanding purpose, we will call your existing health insurance policy as “Base Policy”. Base policies are generally Comprehensive policies. It means, if you already have an existing policy worth Rs.5 Lakhs, then you will be able to claim your medical cost starting from Re.1 to Rs. 5 Lakhs out of this Base Policy.

“Super Top-up Policies” are a slightly different type of policies. We need to opt for a deductible amount first at the time of buying these policies. Suppose you have an existing Base policy of Rs.5 Lakhs; then you can opt for a deductible amount as Rs.5 Lakhs. Then we need to choose Sum Insurance for Super Top-up plans. Suppose you have chosen Sum Insurance under Super Top-up policy as 10 Lakhs, then you have got a total health cover of Rs.15 Lakhs (Rs.5 Lakhs in base plan + Rs. 10 Lakhs in Super Top-up Plans)

But, please pay attention, we will never be able to claim the first 5 Lakhs from our Super Top-up Policy! Let’s understand this with example. If you have incurred the total medical cost of Rs.6 Lakhs then you need to claim 5 Lakhs from your base policy. The Super Top-up Plan will never pay you for the medical expenses of first 5 Lakhs as you have opted for the 5 Lakhs deductible amount. The remaining 1 Lakh will be paid by the Super Top-up Plan. In short, you have recovered your actual medical cost incurred i. e. 6 Lakhs. Any cost, over & above 5 Lakhs but not more than the Sum Insured of your Super Top-up Plan (in this example 10 Lakhs) will be paid by the Super Top-up Plan. Interestingly, the Super Top-up Plans are much economical than Base Policies.

This concept is relatively a new concept. Insurance companies have very little claim experience under these type of plans. But still, this is a very promising concept.

Though the Super Top-up Plans are very economical, it is highly advisable to keep a strong Base Policy with a good company of at least 5 Lakhs to 10 Lakhs.

One more thing, those who can afford to pay the premium for Base policies of 50 Lakhs or 60 Lakhs, it is advisable to buy comprehensive base policies only. Please don’t buy these Top-up plans. Please understand, “Super Top-up Plans” are the budget & economy plans. The facilities offered under these plans are also according to its budget.

Beware of the “Top-up Plans” which are available in the market. In such plans, Deductible amount will be applicable not just once in a year, it will be applicable each time you claim.

Overall, the “Super Top-up Plans” are a good option to increase your family health cover at a very low price. One must buy this plan to secure the family without any delay.